Join us at our Centerville Rd branch on Friday, August 14th from 1 – 4 PM for a summer member appreciation event featuring FREE sweet treats from TJ’s Ice Cream Truck.

Join us at our Centerville Rd branch on Friday, August 14th from 1 – 4 PM for a summer member appreciation event featuring FREE sweet treats from TJ’s Ice Cream Truck.

When you’re dreaming of a new car, a first home, or even a more flexible credit card, there is one number that often dictates how quickly you can reach your goals: your credit score. At WFCU, we believe your financial journey should be navigated with confidence, not confusion. Understanding how your credit score works is the first step toward building a solid financial future. Let’s break down what that number really means and how you can help it grow.

What Exactly is a Credit Score?

Think of your credit score as a type of financial report card. When you apply for a loan, lenders use this number to determine how likely you are to make your payments on time. Your score is calculated based on your credit report, which is a detailed profile of your borrowing history managed by the three national credit bureaus: Experian, Equifax, and TransUnion. This report tracks your accounts, how much you owe, and your payment history.

Why Your Score Matters

A higher credit score doesn’t just help you get “approved,” it saves you money. Members with higher scores typically qualify for lower interest rates and better loan terms.

The Five Pillars of Your Credit Score

Not all financial habits are weighted equally. Most scoring models (like FICO) look at five specific areas:

- Payment history: This is the most significant factor. It looks at whether you’ve paid your bills on time and if you have delinquent accounts or collection items.

- Amounts Owed: This measures your revolving “credit utilization” (how much of your available credit limit you’re currently using), and your account balances.

- Length of Credit History: This refers to how long your accounts have been open and how long it’s been since there was activity on your accounts. Generally, the longer your accounts have been open, the better for your credit score.

- Types of Credit: Lenders like to see a healthy mix of revolving credit (cards) and installment loans (auto or home loans).

- New Credit: This includes the number of credit inquiries and the length of time since a new account was opened. Opening too many accounts in a short window can signal risk and temporarily cause your score to decline.

Simple Steps to Improve Your Score

Improving your score is a marathon, not a sprint, but these habits will help you move the needle in the right direction:

Monitor Regularly

You are entitled to one free credit report per year from each bureau at annualcreditreport.com. Review these reports for errors and dispute any inaccuracies immediately.

Automate Your Payments

Since payment history is the biggest piece of the puzzle, setting up recurring payments from your Wheatland FCU checking account ensures you never miss a due date.

The 30% Rule

Try to keep your credit card balance below 30% of your total limit. “Maxing out” your credit cards significantly lowers your score. Paying down a balance is often the fastest way to see a score increase.

Keep Old Accounts Open

Even if you don’t use an old card frequently, keeping it open helps your “length of history.” Only open new accounts as needed.

Group Your Inquiries

If you’re shopping for a mortgage or auto loan, try to keep your applications within a 30-day window so they are treated as a single inquiry.

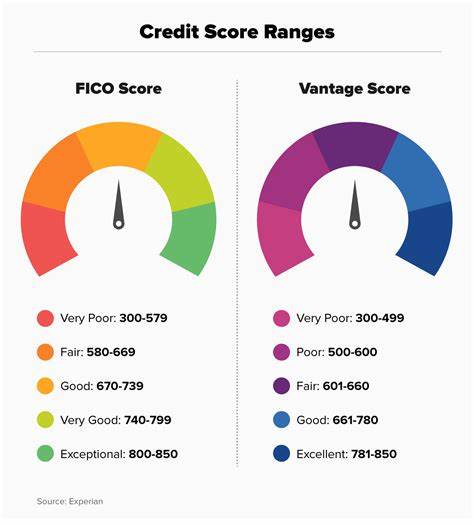

Understanding the Numbers

Credit scores typically fall between 300 and 850, but the chart pictured below shows that the “range” for what is considered good can vary depending on which scoring model is being used.

While there are many different scoring models, the two most common are FICO and VantageScore. FICO is used by the vast majority of lenders (including many credit unions) when making lending decisions. The VantageScore is often what you see when you check your score through free monitoring services or banking apps.

Each model weighs your financial data slightly differently. For example, a score of 785 is considered “Very Good” in the FICO model but falls into the “Excellent” category for VantageScore.

Don’t worry if your scores aren’t identical across different apps. What matters most is the trend. If you’re paying your bills on time and keeping your balances low, both scores will climb together, helping you unlock those better rates and terms.

We’re Here to Help

Wheatland FCU is more than a place to keep your money. We’re your financial partners. If you’re looking to build your credit from scratch or recover from a few bumps in the road, we have services designed for you.

Along with secure checking and higher yield saving options, we also offer free financial counseling for our members. One of our credentialed Financial Counselors can work with you to review your credit and develop a plan to help you meet your goals. Learn more about our free counseling and how to get started.

Every financial journey is unique, and we’re excited to help you navigate yours. Whether you have questions about your report or are ready to apply for your next loan, you can stop by one of our branches or schedule an appointment today.

Resources

Experian

1-888-397-3742

www.experian.com

TransUnion

1-800-916-8800

www.transunion.com

Equifax

1-800-685-1111

www.equifax.com

Source: Federal Reserve Bank of Philadelphia

Recent Blog Posts